YOU HAD ME AT EBITDA 💸 💚

EBITDA has been one of the most (mis)used acronyms across startups, founders and investors. Pronounced as EE-BIT-DAA, it became popular during the leveraged buy-out (LBO) era in the 1980s.

The advocates of LBO promoted this concept for companies which had already invested heavily in their capital expenditures. With no additional expenditure, EBITDA became a proxy for the ability to service debt, and also a measure of cash flow for those companies.

It’s usage evolved to companies which were at a bankruptcy stage and were seeking a turnaround by investors. With time, it has found a universal application across all kinds of companies and has become the single largest analytical measurement tool. This is reflected in its popularity, as the below chart indicates.

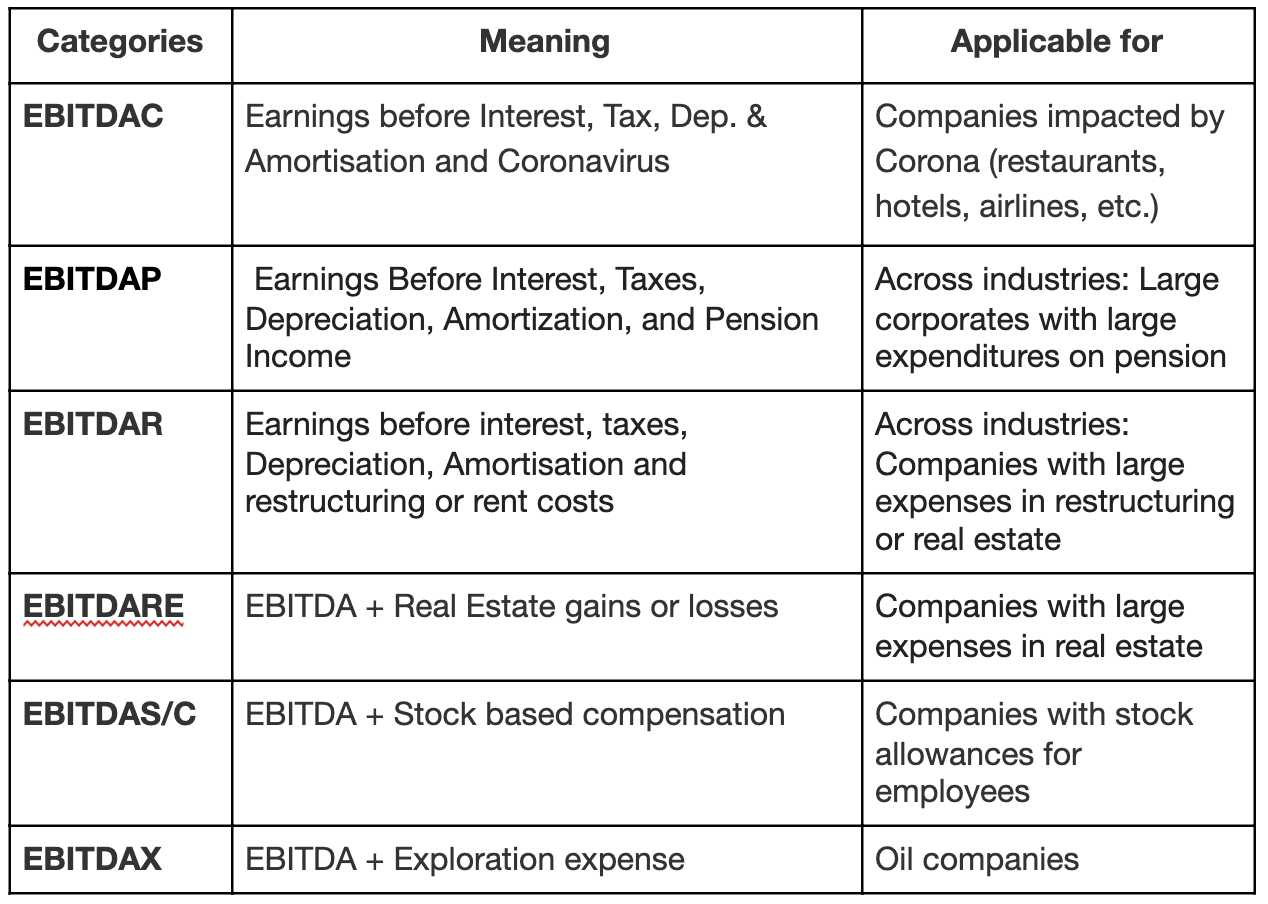

Over time, EBITDA has got numerous flavours of its own. Jason Zweig, a journalist at Wall Street Journal, ticks off some of the other flavours of EBITDA: EBITDAC, EBITDAO, EBITDAP, EBITDAR, EBITDARE, EBITDAS or EBITDASC, EBITDAX.

Adjusted EBITDA

With so much nuance surrounding EBITDA, it is only important for all founders and entrepreneurs not only to understand what it means, but to use it as a fundamental driver of value. In this article, we will see:

EBITDA and its calculation

EBITDA and its usage in the current ecosystem

Adjusted EBITDA and its impact in valuation

Alternatives to EBITDA for measuring valuation

EBITDA and its calculation

A simple way to calculate EBITDA is to take the Net Income and add back Interest, Tax, Depreciation and Amortisation. This applies for companies which publish annual or quarterly results and where Net Income can be obtained easily.

Another approach is to reduce Operating Expenses from Revenue.

EBITDA = Net Income + Interest + Taxes +Depreciation + Amortisation; OR

EBITDA = Net Revenue - Operating Cost

Where (amongst other things):

Depreciation is created when the cost of a long-term asset is divided over its useful life and reported as an expense over a period of time..

Amortization involves expenses with intangible assets such as intellectual property, goodwill or patents.

Essentially, EBITDA measures the financial viability of a business as a standalone entity i.e. without considering the corporate structure (debt and interest expense), country (tax laws) and any long term fixed cost (plants, property & equipment).

The Tech companies usually have similar corporate structure i.e. with minimal or no debt with very less long-term fixed costs, and hence they make it an ideal candidate for EBITDA.

This upward standardization allows an Uber to be compared with Ola to a GrabTaxi to a Gojek. In fact, EBITDA allows companies across different industries to be measured and compared for their operational profitability.

Below is an EBITDA graph of the 5 largest companies in their respective industry.

EBITDA Margins comparison

EBITDA margins show how the operational efficiency of the companies differ according to the industries they are in. As a software company, Facebook has the highest EBITDA, while Amazon has a much lower EBITDA. Uber has a negative EBITDA which reflects its huge costs in its other subsidiaries like Eats, Freight. These comparisons through EBITDA also helps us compare the industries.

With very few moving parts as a metric, and without any additional expenses removed, it does look appealing to shareholders.

Despite the ease of calculation and comparison, the metric has been criticised by the Value Investing community.

As per Warren Buffett,

We won’t buy into companies where someone’s talking about EBITDA. If you look at all companies, and split them into companies that use EBITDA as a metric and those that don’t, I suspect you’ll find a lot more fraud in the former group.

Look at companies like Wal-Mart, GE and Microsoft — they’ll never use EBITDA in their annual report.

People who use EBITDA are either trying to con you or they’re conning themselves. Telecoms, for example, spend every dime that’s coming in. Interest and taxes are real costs.

and to quote Charlie Munger

To make his point about excess, Munger cited the proliferation of EBITDA as a fake profit metric. “I don’t like when investment bankers talk about EBITDA, which I call bulls--- earnings,” he said.

“It’s ridiculous,” Munger said, noting EBITDA — which is short for earnings before interest, taxes, depreciation and amortization — does not accurately reflect how much money a company makes, unlike traditional earnings. “Think of the basic intellectual dishonesty that comes when you start talking about adjusted EBITDA. You’re almost announcing you’re a flake.”

Both Buffett and Munger do have reasons to doubt aspirations on EBITDA as a leading metric for measurement. Reporting only EBITDA can be misleading as it has been used to hide expenses on huge debt interest, or even on fixed capital and depreciation. This is what WorldCom did to hide the $3.8 billion charges on debt and other expenses.

Worldcom was not alone. In the 1980s, Waste Management changed their depreciation schedule from 5 to 8 years to inflate their earnings. This inflated the profits, as less depreciation expenses were charged. Similarly, Boeing extended the depreciation schedules of its 737 airlines, thereby reducing the overall expenses and increasing profitability.

For industries which require huge investments in Plant, Property & Equipment, it would be incomplete to look at EBITDA for a Telecom, Manufacturing or Logistics firm since they pour massive amounts of capital in fixed investments and write down depreciation every year.

The warning here is: EBITDA cannot be relied on as a sole determinant of value. The value for a company needs to be looked holistically.

A due diligence of a company should holistically look at its market size, team, growth rate, quality of revenue, intellectual property, customer concentration which are more important than EBITDA.

EBITDA and its usage

For Tech companies, however, EBITDA is still the go-to metric to estimate value.

This is also because estimating valuation through traditional means for startups can get complex and extremely subjective, especially in today’s uncertain world.

Put simply, the EBITDA of a company is multiplied by a multiple (a multiple is the company value divided by the metric i.e. EBITDA) to calculate the enterprise value. The multiple is an indicator of how many times of EBITDA one has to pay, if they acquire the business (or enterprise) and is usually dependent on potential market size, growth rate, profitability, team, etc.

EBITDA multiple has a cousin in Revenue multiple (EV / Revenue) that is often used to measure value. Entrepreneurs often miss the interconnection between the revenue and EBITDA multiple.

In other words, if a company has an EBITDA margin of 30% and the overall value of the company is at, say 10x of EBITDA, the revenue multiple would be 30% * 10x = 3x of Revenue.

This triangulation and validation helps when we have market info only for one multiple.

Adjusted EBITDA and its impact in Valuation

The concept of adjusted EBITDA has been prevalent - since the early 2000s as it enhances the attractiveness of the company by taking out one-time adjusted expenses.

These one-time expenses have no bearing on the company’s operational or business costs and often the argument is to make the EBITDA normalised by removing non-recurring, irregular and one-time items.

These adjustments are usually one-off costs / charges and the argument is to make the EBITDA normalised by removing non-recurring, irregular and one-time items that may distort the real picture.

The formula for adjusted EBITDA is

Adjusted EBITDA = EBITDA + One time Expenses

Some of the ways in which EBITDA can be adjusted are:

Adjustments across the P&L

Revenue - Inability to fulfill orders or cancellation of orders especially due to Covid.

Cost of Goods sold -one-off increased costs e.g. Covid precautionary measures, additional freight expenses, alternate suppliers, etc.

Operating Expenses -one-off changes in sales commissions, labor charges, advertising costs etc.

Run-rate Revenue / EBITDA

Used more often, this approach looks at the revenue or costs for a shorter period of time and is annualised to 12 months to show how the growth or expense would look like. It is a good estimate especially in periods of uncertainty when forecasting a full-year period is cumbersome.

Normalised Revenue / EBITDA

In this method, the months which are severely impacted by any calamity say, a flood or a pandemic are replaced by last year’s revenue. Starting from a normalised revenue, companies usually build out a normalised EBITDA.

These methods or tools should be used with extreme caution. Often, the revised costs or revenue that are shown as one-off may recur if the underlying situation continues and the world has actually shifted. Example - The current Covid scenario continues unabated is a reflection of the times that the world might have changed for a medium term future (at least until a vaccine is discovered) hence, Covid adjustments might not make sense.

We have seen WeWork using “Community adjusted EBITDA,” which drew a lot of flak from the financial press. The community adjusted EBITDA only looked at the location or unit based operating costs and expenses and removed any advertising, marketing and development and design costs for the locations which were currently being built.

In other words, the Customer Acquisition Costs were treated as non-operating expenses. This indicated that the company is profitable from a unit economics perspective. It is, however, another matter that the loans of credit of $ 1 billion (and their interest) could not be figured out only by looking at the community adjusted EBITDA.

Alternatives to EBITDA for measuring Valuation

EBITDA should be complemented with business metrics to understand a company’s performance.

Some of the other metrics to measure performance are:

Revenue muliple - Multiple of revenue, example shown above. Applicable to Technology companies

P/E ratio - also known as price or earnings multiple, it is the ratio of price per share to earnings per share, though mostly applicable to publicly listed companies

DCF - Discounted Cash flow method which estimates the cash flows provided by the company discounted to the present value

Customer Lifetime value method - a bottom up approach to valuation by estimating the customer value and also the no. of customers that a company gets. The resultant product is the valuation of the company.

While the usage and popularity of EBITDA is not debated, rather than looking at EBITDA as a hammer to solve all company valuation problems, it should be looked as one of the tools in conjunction to measure value.